Unlock Your Home: No Interest Furniture Financing

You finally find the piece that makes the room click. Maybe it’s a sectional designed for family movie nights, a new dining set for holiday dinners, or a mattress that feels right the second you lie down. Then you look at the full price and think, “I want this, but I don’t want to strain the budget.”

That’s where no interest furniture financing enters the picture. Used carefully, it can give you breathing room without forcing you to settle for furniture that doesn’t fit your home or your life.

For many households, that choice is normal, not unusual. Nearly one-third of recent U.S. furniture buyers used financing options, including no-interest-if-paid-in-full plans, according to the Provoke Insights Furniture Consumer Trends report. That tells you something important. People aren’t only financing because they’re careless. They’re often financing because furniture is a high-consideration purchase that affects daily comfort, family routines, and long-term value.

If you’ve ever paused before buying because you wanted to “think it over,” that’s a smart instinct. This guide on why furniture purchases are high-consideration decisions captures that feeling well. Furniture isn’t a casual buy. It’s a home decision.

Since 1936, our neighbors in Norwich have walked into the showroom with the same question in different forms. “Can I get the piece I really want without upsetting the rest of my finances?” The answer is often yes, but only if you understand how the financing works before you sign.

Bringing Your Dream Home to Life Sooner

A lot of local shoppers reach the same moment.

They’ve narrowed down styles. They’ve sat on the sofa. They’ve compared fabrics. They’ve pictured a custom F9 Custom Sofa in the living room instead of the worn-out one they’ve been meaning to replace for years.

Then the practical side kicks in. The room needs the upgrade now, but paying the whole amount at once may not be the smartest move this month.

That’s why no interest furniture financing can be useful. It lets you spread a major purchase into manageable payments while keeping cash available for the rest of life. Rent or mortgage, groceries, school costs, car repairs, all of that still exists after the furniture arrives.

Why shoppers use financing for furniture

People often think financing means “buying more than I should.” In many cases, it really means “buying thoughtfully.”

A few common reasons shoppers choose it:

- They want better quality now. A well-made sofa, dining set, or mattress often serves a home much longer than a quick replacement buy.

- They’re furnishing after a move. New rooms need essentials fast, not one piece every few months.

- They’re balancing priorities. Paying over time can help a family improve the home without draining savings.

- They’re ordering custom. Personalized pieces like Canadel dining or the F9 Custom Sofa are often worth planning for, not rushing into.

Furniture financing works best when it helps you buy intentionally, not impulsively.

For many Eastern CT households, the appeal is simple. You don’t have to wait until the “perfect financial month” to make your home more comfortable and functional.

The real benefit

The biggest advantage isn’t just delay. It’s control.

When the payment schedule fits your budget, you can choose the piece that suits your lifestyle instead of the one that only fits today’s cash on hand. That might mean a dining set that works for your space long term, or a mattress that supports healthier sleep instead of another temporary compromise.

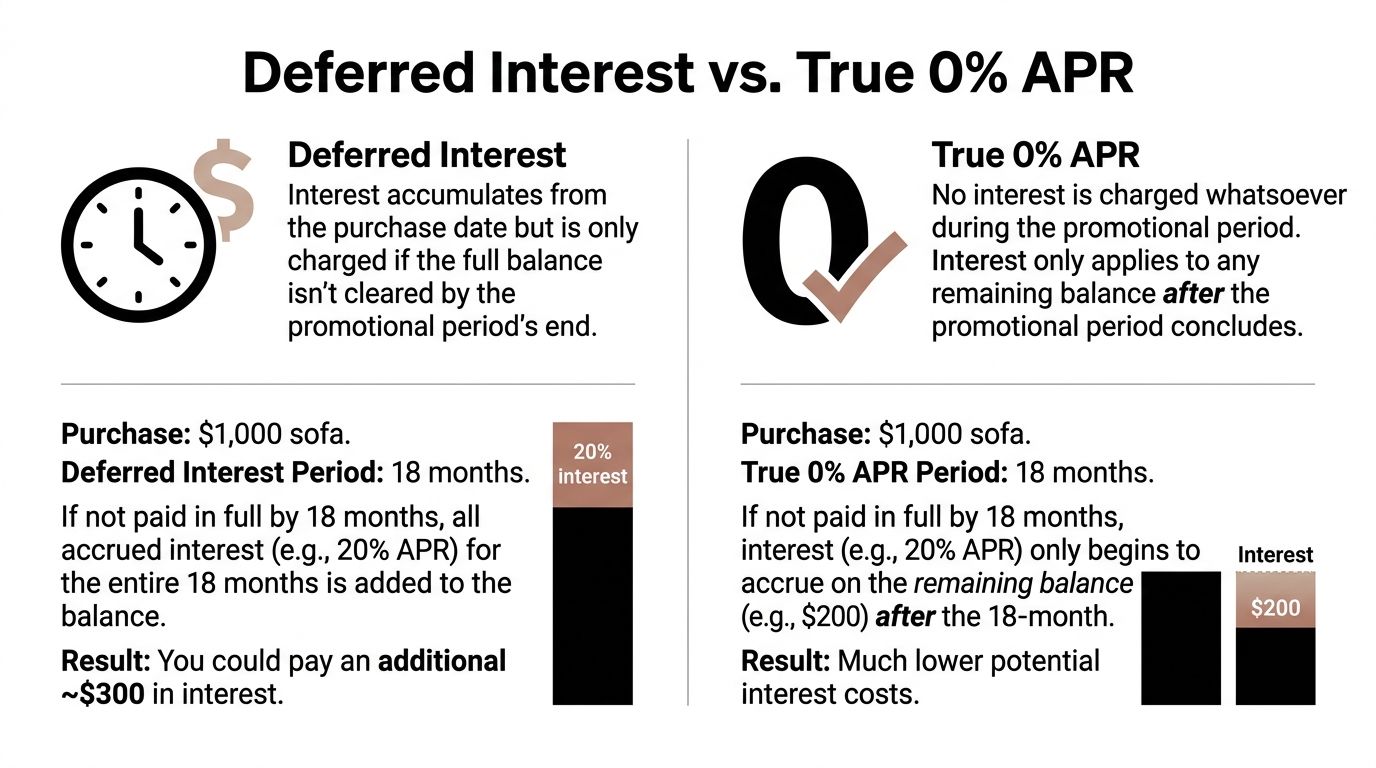

Understanding Deferred Interest vs True 0% APR

A lot of Norwich shoppers hear “no interest” and assume every offer works the same way. At Gorins, that is usually the moment we slow things down and look at the fine print together, because the difference between deferred interest and true 0% APR changes how you plan your payments from day one.

Deferred interest means the interest is waiting in the background

Deferred interest works like a bill that stays covered as long as you finish on time. If you pay the full balance before the promotion ends, that interest never gets added. If you still owe even a small amount at the deadline, the lender may charge interest back to the original purchase date.

That is the part shoppers often miss. The monthly payment can look comfortable, but the essential question is different. Will this payment get the balance to zero before the promotion ends?

The Consumer Financial Protection Bureau explains that deferred interest promotions can apply interest from the purchase date if the balance is not paid in full by the end of the promotional period, as described in its overview of deferred interest and similar financing offers.

True 0% APR means no interest during the promo period

A true 0% APR offer is more straightforward. No interest is charged during the promotional window. If you still have a balance after that period ends, interest usually starts at that point on the remaining balance, rather than reaching back to day one.

For many families around Norwich, that setup feels easier to follow because there is less guesswork. You still need a plan. But the rules are clearer.

Why the difference matters with Gorins financing options

If you are looking at a Nest Card or a TD Bank offer at Gorins, do not stop at the words “special financing.” Ask which type of promotion it is, how long the promotional period lasts, and what payment amount gets you to zero on time. That short conversation can save a lot of confusion later.

Here is a simple way to compare what you are seeing:

| Plan type | What to ask | What to watch |

|---|---|---|

| Deferred interest | “If I miss the payoff date, does interest go back to the purchase date?” | Backdated interest charges |

| True 0% APR | “When does interest begin if I still have a balance?” | The regular rate after the promo period |

| Equal monthly payment plan | “Is this payment enough to fully pay it off by the deadline?” | Payments that are too low to finish on time |

A good furniture plan starts with a good shopping plan. If you are still comparing room needs, sizes, and budget tradeoffs, this guide on how to shop for furniture smartly can help you make the financing choice fit the purchase, not the other way around.

If you are already balancing other monthly obligations, it also helps to review practical payoff habits like the ones in this guide on how to pay off debt fast.

Simple rule: If the offer says “paid in full by the deadline,” treat that date like the real finish line.

How Retroactive Interest Charges Can Derail Your Budget

A Norwich shopper picks out a sofa, a rug, and a bedroom set at Gorins, signs up for a promotional financing offer, and makes payments every month. A year later, there is still a small balance left. That leftover amount can turn an affordable plan into a much more expensive one.

That is how retroactive interest works on a deferred interest promotion.

What happens when the deadline passes

With this type of offer, the key date is not the last statement date you happen to notice. It is the promotional payoff deadline. If the balance is not fully paid by then, interest can be charged from the original purchase date, not just from the day after the promotion ends. The Consumer Financial Protection Bureau explains this risk in its guidance on deferred interest promotions.

A simple way to view it is this: deferred interest works like a timer running in the background. While the promotion is active, that timer does not cost you anything if you finish on time. If even a small amount remains at the end, the lender may add interest based on the full promotional terms.

That surprise is what throws off a household budget.

Why shoppers get caught by it

This usually does not happen because someone ignored the bill. It happens because the monthly payment and the payoff plan were not the same thing.

A few common examples:

- The required minimum payment was lower than the amount needed to finish on time.

- One payment posted late and shortened the cushion at the end.

- Another home expense took priority for a month or two.

- The shopper assumed a small remaining balance would not matter.

At Gorins, this is one of the biggest points worth slowing down for with Nest Card or TD Bank offers. The furniture choice may feel like the big decision, but the payment schedule is what decides whether the promotion saves you money or adds cost.

A deferred interest deadline is closer to a final due date than a suggested target.

If you are juggling several balances at once, a broader payoff strategy can help you protect that deadline. A resource on how to pay off debt fast can help you sort which payments need the most attention first.

The safer question to ask before you sign

Ask this at the showroom or before you complete the application online:

“What payment gets me to zero before the promotion ends?”

That question gets you closer to the actual cost than asking for the minimum payment. Minimum payments keep the account in good standing. They do not always clear the balance before the deferred interest date.

It also helps to build your purchase plan carefully before financing enters the picture. Our guide to the dos and don'ts of furniture shopping can help you match the right pieces, price range, and payment plan so there are fewer surprises after delivery.

What Lenders Look For and How It Affects Your Credit Score

Most shoppers worry about approval in a very general way. “Will I qualify?” is usually the first question.

A better question is, “What are lenders checking? ”

The score ranges that often matter

For no interest financing, qualification thresholds often require a FICO score of 640+ for 12-24 month terms and 700+ for longer 36-60 month terms, according to this summary of furniture financing credit requirements.

That doesn’t mean approval is based on one number alone. Lenders may also consider your existing debt, payment history, and how much available credit you’re already using.

Still, those ranges give shoppers a practical starting point. If you’re aiming for a longer promotional term, stronger credit usually gives you more room.

Soft pull and hard pull in plain language

This part confuses people all the time.

- Soft pull: A pre-qualification check that doesn’t carry the same impact as a formal application.

- Hard pull: A full credit inquiry tied to an application for new credit.

Knowing the difference matters because some shoppers want to explore options before committing.

If you want a simple outside explanation, this primer on how credit scores are calculated breaks down the basics in easy language.

Can financing help your credit too

It can, if you handle it well.

The same source notes that on-time payments can potentially raise scores by 20-40 points over the long term through improved credit utilization and positive payment behavior. That doesn’t happen overnight, and it isn’t automatic. It depends on paying consistently and keeping the account under control.

Financing can support your credit, but only when the payment plan fits your real budget.

If you’re early in the shopping process, understanding the furniture buying journey from first research to final decision can help you line up style, budget, and financing before you apply.

Applying for Your Nest Card or TD Bank Offer in Norwich

The application process feels much easier when you know what to expect before you walk in.

Shoppers usually come in focused on the furniture first. They’re comparing a Canadel dining setup, trying reclining comfort, or testing mattresses in the Sleep Gallery by feel. Once the product choice starts to narrow, financing becomes part of the conversation.

What the in-store process usually looks like

The steps are pretty straightforward.

Choose the piece or narrow the options

It’s easier to evaluate a financing offer when you know whether you’re buying one item, a room group, or a custom order.Ask which promotional plans apply

Some offers are tied to specific purchase ranges, terms, or credit approval standards. Paying close attention to details is essential.Review the type of financing carefully

You want to know whether the offer is no interest if paid in full, equal monthly payments, or another structure.Complete the application

A team member can walk you through the form and help you understand what information is needed.Read the payoff terms before finalizing

Focus on the deadline, required payment amount, and what happens if a balance remains.

Where the Nest Card and TD Bank fit in

At Gorins Furniture & Mattress, shoppers may use financing options connected to the Nest Credit Card and certain TD Bank offers, depending on approval and the promotion available at the time. In practical terms, these options can help someone bring home a custom dining set, a Flexsteel sofa, or a mattress from Tempur-Pedic, Serta, or Beautyrest without paying the full amount upfront on day one.

The key is matching the financing structure to the purchase.

- A custom Canadel dining set may call for a payoff schedule you can map clearly from the start.

- A Sleep Gallery purchase may feel more urgent if your current mattress is affecting rest.

- A living room order with thousands of customization paths, like the F9 Custom Sofa series, often benefits from planning the payment before finalizing the fabric and configuration.

Questions to ask while you’re standing there

Not every customer asks these, but they should.

- “Is this deferred interest or a true 0% APR structure?”

- “What payment gets me to zero before the deadline?”

- “Is pre-qualification available?”

- “What happens if I pay it off early?”

Those questions make the conversation calmer because they replace guesswork with specifics. And if you’re furnishing more than one room, it’s smart to decide whether the financing is helping you stay organized or tempting you to overextend.

Calculating Payments to Ensure You Finish On Time

This is the part that keeps no interest furniture financing working in your favor.

You don’t need complicated math. You need one simple formula and the discipline to use it.

The easiest payoff formula

Use this:

Total purchase amount ÷ number of promotional months = target monthly payment

That gives you the payment that should get you to zero by the end of the promotion, assuming you stay on schedule.

For example, if you finance a bedroom or living room purchase and the term gives you a fixed number of months, divide the total by that month count before you look at the minimum due. Your target payment is the number that finishes the job. The minimum due may only keep the account active.

A safer way to set the payment

Many shoppers do best when they add a little cushion.

You can:

- Set up autopay so you don’t miss the due date

- Round up the monthly payment to reduce the chance of a small leftover balance

- Check the balance before the final month so there’s time to correct any gap

The point isn’t perfection. The point is avoiding the last-minute surprise that turns a good promotional plan into an expensive one.

Match the payment to your real month

Before you commit, ask yourself:

- Does this fit after fixed bills?

- Will seasonal expenses interfere?

- Am I planning around minimums or around payoff?

That last question matters most.

If the payoff number feels tight on paper, it usually feels tighter in real life.

For shoppers reworking a full room on a budget, ideas like these budget bedroom makeover ideas can help you decide where financing makes sense and where a simpler upgrade may be smarter.

Frequently Asked Questions at Our Norwich Showroom

Can I use financing on custom furniture

Often, that depends on the current promotion and the purchase details.

A shopper asking about a custom Canadel order or an F9 Custom Sofa should ask about financing before finalizing options. It’s much easier to design confidently when you already understand the payment structure.

Can I pay it off early

Many shoppers ask this right away, especially people who expect a tax refund, bonus, or upcoming home sale.

The important thing is to verify the terms on the specific offer. Early payoff can be helpful because it reduces the chance of carrying a balance to the promotional deadline.

How fast does approval happen

That can vary by lender and offer. In many cases, the process is designed to be straightforward enough that shoppers can review their options while they’re still making the purchase decision.

If timing matters, say so. A delivery deadline, move-in date, or mattress replacement need can affect how you want to proceed.

Is financing only for large room packages

No. Some shoppers use it for a single mattress, recliner, or dining purchase.

Others use it for larger projects because they’re furnishing multiple rooms at once. The right use depends less on the size of the order and more on whether the payment plan is clear and manageable.

Should I finance if I could pay cash

Sometimes yes, sometimes no.

If financing helps you preserve savings and you know you can complete the payoff on time, it may be a practical tool. If the deadline feels uncertain, cash or a smaller purchase may be the better path.

Since 1936, Gorins Furniture & Mattress has helped Norwich and Eastern CT families create homes they love. From custom-designed Canadel dining sets to the latest in Tempur-Pedic sleep technology, we combine a massive selection with the personalized care only a local, family-owned business can provide. If you’d like help comparing financing options in plain language, visit the Norwich showroom at Gorins Furniture & Mattress, take the online Style Quiz, or browse the Clearance section for value-driven savings.