Buy Now Pay Later Furniture: A Norwich Shopper’s Guide

A shopper in Norwich finally finds the right sofa. The scale is right, the fabric works with the rug, and the seat feels comfortable enough for long movie nights. Then the practical question shows up. How should that purchase be paid for without putting strain on the household budget?

That question comes up often with buy now pay later furniture. It also comes up with dining sets, mattresses, recliners, and room packages. A beautiful piece can feel like the easy part. The payment plan is where many shoppers slow down, especially when checkout pages offer several choices that sound similar but work very differently.

Furniture is a long-use purchase. Payment decisions deserve the same careful attention as wood finish, cushion support, or mattress feel. A short-term installment plan can make sense in some situations. A more structured financing option can fit better in others. The key is knowing what each plan really asks from the shopper.

Table of Contents

- Your Dream Furniture Is Here So How Do You Pay For It

- Understanding How Buy Now Pay Later Works

- The Pros and Cons of Using BNPL for Furniture

- Applying for BNPL and Tips for Responsible Shopping

- Gorins Promotional Financing A Value Driven Alternative

- Your Questions About Financing Your Furniture Answered

Your Dream Furniture Is Here So How Do You Pay For It

A common scene plays out like this. A couple has been making do with a loveseat that's too small, or a renter is ready to replace a hand-me-down dining table with something that fits the apartment and daily routine. The right piece appears, but the full price all at once feels heavier than expected.

That's why buy now pay later furniture has become part of everyday shopping language. Buy now, pay later is no longer a tiny niche. BNPL providers originated about $160 billion in consumer credit products in 2025, and over 60% of issuance carried 0% APR, according to Numerator's summary of Federal Reserve BNPL market insights. For shoppers, that can sound simple and reassuring. Split the bill, bring the furniture home, and spread the cost out.

Why furniture buyers pause at checkout

Furniture isn't an impulse category in the same way small accessories can be. A sofa affects comfort every evening. A dining set shapes how family meals work. A mattress changes sleep quality night after night. The emotional side says yes quickly. The budget side asks tougher questions.

Some households use installments to protect cash flow rather than because they can't pay in full. Others want to keep room in the budget for delivery, decor, or a second piece. Shoppers who are also planning curtains, lamps, or a fresh layout sometimes benefit from practical planning tools like this affordable living room makeover guide, which helps connect the furniture purchase to the bigger room budget.

Furniture should feel settled before it feels financed. A smart plan supports the room instead of creating stress around it.

The local question behind the financing question

In a long-standing local showroom, financing conversations usually sound less like checkout marketing and more like design planning. Since 1936, local furniture guidance in Norwich has often started with the same concern. What fits the home, and what fits the monthly budget without regret later?

That's also why timing matters. Some shoppers do better when they wait for the right promotion, the right season, or the right clearance opening rather than rushing into the first payment plan they see. A useful starting point is this guide on the best time to buy furniture, because the smartest financing choice often begins with the smartest purchase timing.

Understanding How Buy Now Pay Later Works

BNPL is a short-term installment plan. The shopper takes the furniture home now and pays for it in scheduled parts rather than one single payment. Most confusion starts because the checkout language sounds easy, but the timing and structure matter a lot.

The standard retail structure is usually a $50 to $1,000 purchase split into four equal installments, with the first payment due at checkout and the remaining payments due at two-week intervals over six weeks, based on the Consumer Financial Protection Bureau's BNPL market report. That setup is often called pay in 4.

A simple way to picture pay in 4

A shopper buys an accent chair priced within that typical BNPL range. Instead of paying the full amount that day, the cost is divided into four equal parts. One part is paid immediately. The other three are charged automatically on the scheduled dates.

That automatic part matters. Many shoppers think only about the first payment because it's the amount they see at checkout. The commitment is the full sequence of charges already lined up behind it.

Terms that often get mixed up

A few definitions help clear the fog:

- Installment means one scheduled payment in a series.

- APR means annual percentage rate. If a plan says 0% APR, it means no interest is charged under that agreement's terms.

- Down payment is the amount due right away. In a pay-in-4 setup, the first installment functions like that immediate upfront payment.

- Automated payment means the future charges are usually pulled automatically from the card or account connected at checkout.

Practical rule: If the buyer can't comfortably cover all four payment dates from known income, the price probably isn't a fit for short-term BNPL.

How BNPL differs from other ways to pay

BNPL is not the same as layaway. With layaway, the shopper usually finishes paying before taking the item home. BNPL allows immediate possession while the payments continue.

It also doesn't work exactly like a general-purpose credit card. BNPL is tied to a specific purchase and a fixed repayment schedule. For readers who want a category overview of stores and setups built around these plans, this page on furniture stores that accept Afterpay gives additional context without changing the core mechanics described above.

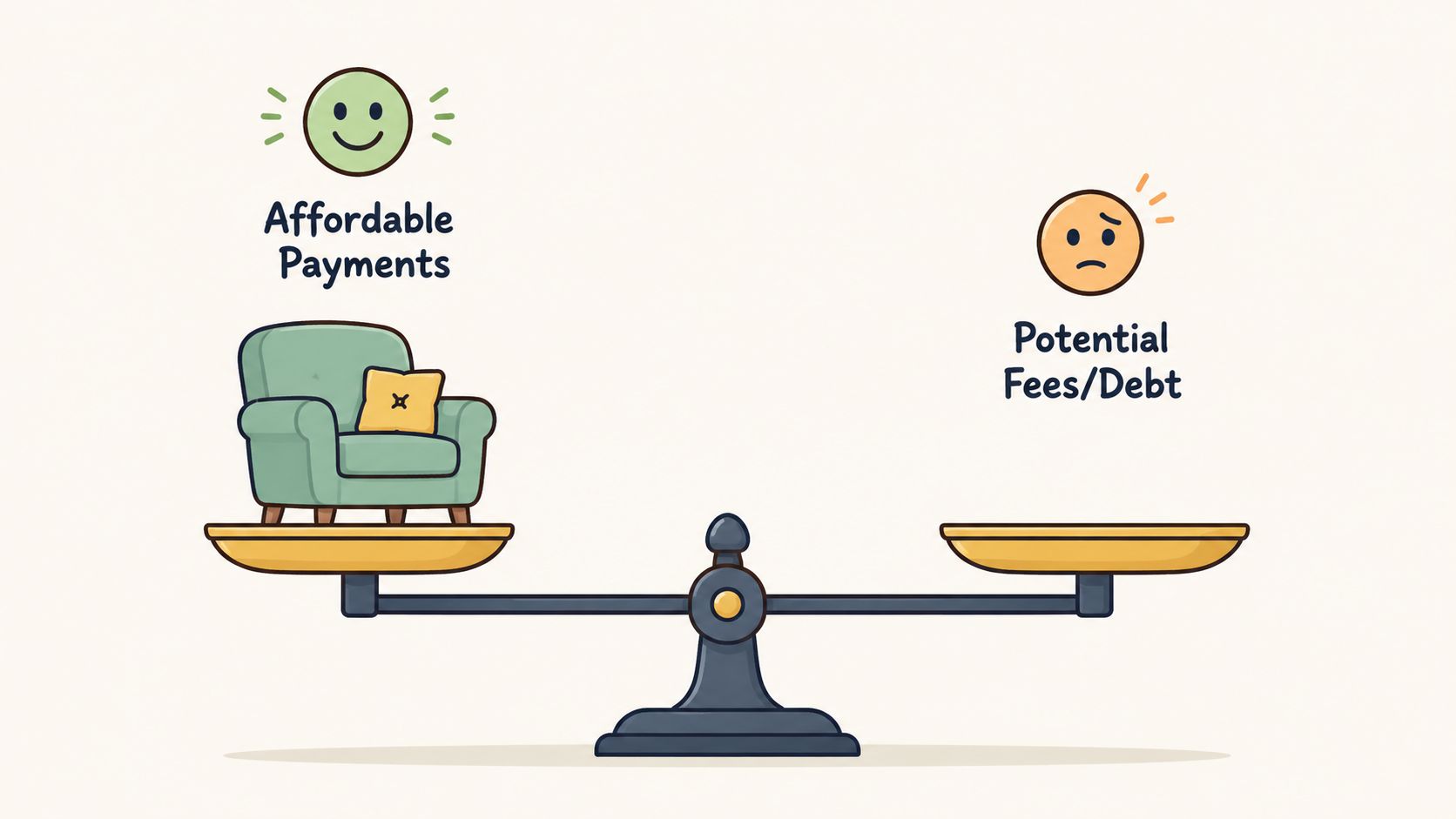

The Pros and Cons of Using BNPL for Furniture

BNPL can be helpful. It can also cause problems when the repayment pace doesn't match real life. Furniture makes that tradeoff more serious because the ticket is often larger than clothing or small electronics, and the product itself is meant to stay in the home for years.

Where BNPL helps

For the right buyer, buy now pay later furniture can reduce upfront pressure.

- Cash-flow breathing room helps when a household needs the piece now but wants to spread the cost across several pay periods.

- Fast checkout can feel less intimidating than a longer credit application.

- Clear installment dates may help disciplined shoppers plan around payroll timing.

- Immediate use matters with practical purchases like a mattress, bed frame, or dining set needed for daily living.

A renter moving into a first apartment is a good example. If the room is empty and the basics are needed quickly, installment payments can smooth out the purchase without requiring the full amount on day one.

Where shoppers get caught off guard

The same simplicity that makes BNPL attractive can also hide risk.

A short payment window can feel manageable until it overlaps with utilities, groceries, car repairs, or another installment purchase. A shopper may approve the first payment comfortably but feel squeezed by the third and fourth. The furniture may already be in the room, but the budget pressure is still unfolding.

Another issue is that many pages talk about monthly affordability while skipping the bigger question of total agreement cost and what the buyer owns under the terms. Miller Waldrop's discussion of furniture financing for bad credit warns that shoppers should compare the full agreement cost, because some plans are promotional retail credit while others are lease-to-own structures with very different economics.

The better comparison to make

The useful comparison isn't just “Can the first payment be handled?” It's this:

| Question | Why it matters |

|---|---|

| Can every scheduled payment be covered on time? | A tight schedule can become stressful fast. |

| Is the agreement actual financing or another structure? | Ownership and total cost can differ. |

| What happens if the item is returned or delayed? | Furniture has delivery and fit complications. |

| Does the plan match the size of the purchase? | A lamp and a room package don't belong in the same repayment logic. |

A good furniture payment plan should make the room feel more livable, not make the next six weeks feel crowded.

Applying for BNPL and Tips for Responsible Shopping

The application process for BNPL is usually built right into online checkout. The shopper selects the installment option, enters basic personal details, and links a payment method. The main appeal is speed. The decision often arrives quickly, which is convenient but also easy to rush through.

Furniture and home decor are already a major use case for these plans. The Federal Reserve's BNPL overview notes that 26% of BNPL users financed furniture and home decor in the past year, and that category sits among the top BNPL uses, as summarized in the Federal Reserve BNPL product overview. That means many households are making this choice. It also means many households need a better checklist before clicking approve.

What to check before submitting

The smartest shoppers slow the process down for a few minutes and review the terms in plain language.

- Payment calendar: Write down every due date before completing the order.

- Late-fee terms: Read what happens if a payment misses by a day.

- Return handling: Furniture returns can be slower than small parcel returns.

- Delivery timing: A delayed sofa can create frustration if payments have already started.

- Room fit: Confirm dimensions, entryways, stairs, and elevator access before financing begins.

A responsible way to use BNPL

A simple rule works well. BNPL should fund a planned purchase, not create one.

That means the shopper already knows the item is needed, already knows where it will go, and already has room in the budget for every installment. A household that benefits from visual budgeting may find tools like Koru's family debt management helpful for laying out payment timing alongside other obligations.

For in-store and online furniture planning, this practical article on the dos and don'ts of furniture shopping also helps buyers think through size, purpose, and long-term value before financing enters the picture.

Short-term financing works best when the furniture decision is already settled. Financing shouldn't be the reason the purchase suddenly feels acceptable.

Gorins Promotional Financing A Value Driven Alternative

Short-term BNPL works best for relatively contained purchases. Furnishing a full room usually asks for a different rhythm. A custom dining set, a better-built sofa, or a premium mattress often deserves a payment structure that feels steadier and easier to predict month by month.

That's where promotional financing can be easier to live with than a six-week installment schedule. A market projection cited by Market Data Forecast's U.S. BNPL report says 72% of Americans plan to use BNPL in the coming year, with furniture named as a top category. The more common this behavior becomes, the more important it is for shoppers to distinguish between fast checkout financing and structured home-furnishing financing.

Why longer structure can fit furniture better

Furniture is tied to use over time. Payment plans that extend in a more orderly way can feel better matched to that reality.

A household comparing options for a dining room, living room, or mattress purchase may prefer:

- Equal monthly payments instead of payments every two weeks

- More breathing room for a larger total purchase

- Clear promotional terms that are easier to map into the monthly budget

- A better fit for custom or premium pieces that are chosen carefully rather than bought quickly

For significant purchases, that structure often aligns better with how people furnish homes. They choose once and expect to live with the result for a long time.

Where a local showroom option fits

One option in this category is promotional financing at Gorins Furniture & Mattress. It's built around equal monthly payments and promotional financing programs for furniture and mattress purchases, subject to credit approval. That type of setup is often easier to pair with investment-grade selections such as Canadel custom dining, the F9 Custom Sofa approach, or mattresses chosen in person by feel from brands such as Tempur-Pedic, Serta, and Beautyrest.

Since the store has served Norwich and surrounding Eastern CT communities since 1936, the financing conversation sits alongside design guidance rather than replacing it. The same shopper deciding between fabric textures, table shapes, or mattress comfort can also compare payment structure with the same level of care.

The right financing option should match the life of the furniture, not just the speed of checkout.

Your Questions About Financing Your Furniture Answered

Financing questions are often less about math than about confidence. Shoppers want to know whether a plan fits the purchase, whether the process will feel manageable, and whether a better path exists for a larger room project.

What's the difference between BNPL and promotional financing

The biggest difference is usually the repayment pace. BNPL often centers on a short installment sequence. Promotional financing is usually built for a longer horizon with equal monthly payments.

That matters more with furniture than with many other retail categories. A single accent piece might fit a short-term installment plan. A full bedroom refresh, a custom dining order, or a premium mattress upgrade often fits better with a steadier monthly schedule.

Does every furniture purchase belong in BNPL

No. Smaller, planned items can fit that structure well. Larger purchases deserve more scrutiny.

A helpful rule is to match the financing tool to the purchase type:

- Short-term need, smaller scope: A compact installment plan may work.

- Room project or custom order: A monthly structure may be easier to manage.

- Uncertain fit or delivery details: Pause until dimensions, timing, and return terms are fully understood.

What should shoppers ask before signing anything

These questions usually uncover the answer quickly:

- What is the full agreement cost?

- When does the first payment begin?

- How many payments are there, and when are they due?

- What happens if the item is returned, delayed, or doesn't fit?

- Does this plan support the household budget comfortably, not just today, but through the full payment schedule?

For shoppers who are sorting through financing with past credit challenges, this guide on the best place to finance furniture with bad credit offers added context around approval expectations and practical planning.

Since 1936, Gorins Furniture & Mattress has helped Norwich and Eastern CT families create homes they love. From custom-designed Canadel dining sets to the latest in Tempur-Pedic sleep technology, the store combines a massive selection with the personalized care only a local, family-owned business can provide. Visit today to experience quality, value, and 5-Star Delivery service. Shoppers who want to start from home can also take the online Style Quiz.

For neighbors comparing buy now pay later furniture with longer-term payment options, the smartest next step is to see the choices in person and ask clear questions before committing. Visit Gorins Furniture & Mattress in Norwich, take the online Style Quiz, or browse the Clearance section to find a purchase and payment approach suited to your lifestyle.