90 Days Same as Cash Furniture: A Norwich Shopper’s Guide

A Norwich shopper spots the right sofa, the one that fits the room, the style, and the way the family lives. The cushions feel supportive. The fabric works with the wall color. The size is right for movie nights and visiting relatives. Then the price enters the conversation, and the excitement gets quieter.

That hesitation is normal. Furniture is a home purchase, not an impulse buy. A dining set, mattress, or custom sectional should feel like a smart step, not a source of pressure. That's why so many local shoppers ask about 90 days same as cash furniture offers. Used wisely, they can create breathing room between the day a piece comes home and the day the balance is paid off.

Your Dream Furniture Is Within Reach

For many of our neighbors in Norwich, the decision isn't whether a room needs attention. It's whether now is the right time to act. A family may need a new mattress before guests arrive. A renter may finally be ready to replace a hand-me-down loveseat. A homeowner may find the perfect dining set but want to avoid draining savings all at once.

That's where a short promotional financing window can help. Instead of treating financing like a last resort, smart shoppers often use it as a planning tool. They match the purchase to a clear payoff plan and keep the rest of the household budget steady. For readers who want help thinking through the bigger picture, Fintrack's personal finance insights offer a useful overview of how to organize spending around real-life goals.

Why this matters in a furniture showroom

Furniture purchases are emotional and practical at the same time. A sofa changes how a family gathers. A bed changes how someone sleeps. A dining table becomes the place where school projects, takeout dinners, and holiday meals all happen.

Since 1936, Gorins has served Norwich as a locally owned, family-operated business with a simple mission: help families make home decisions with confidence. That same spirit matters when financing enters the discussion. The point isn't pressure. The point is clarity, value, and a path toward investment-grade quality that feels suitable for your lifestyle.

A shopper who wants to prepare before stepping into the showroom can also review smart furniture shopping guidance. A little planning makes the financing conversation much easier.

The best financing offer is the one a shopper fully understands before signing.

What Does 90 Days Same as Cash Really Mean

The phrase sounds simple, but it causes a lot of confusion. Many shoppers hear “same as cash” and assume it means no interest under any circumstance. That isn't always how these promotions work.

The pause button idea

A good way to picture it is a pause button on interest. During the promotional period, the account may be tracking interest in the background, but that interest stays set aside for the moment. If the shopper pays the entire promotional balance by the deadline, the set-aside interest doesn't get charged.

If the full amount isn't paid by the end of the term, the result can be very different. Interest may be added based on the promotion terms, which is why reading the agreement matters so much.

Deferred interest means interest may be held back during the promotional window, then charged if the balance isn't paid in full by the deadline.

Where shoppers get tripped up

The confusion usually comes from one small assumption. Many people believe making the minimum payment is enough to avoid interest. It usually isn't. Minimum payments help keep the account current, but they may not eliminate the full promotional balance in time.

That's why a shopper considering buy now, pay later furniture options should ask one direct question before agreeing to anything: “What exact amount needs to be paid, and by what exact date, to avoid interest?”

A clear answer should include:

- The promotional deadline so there's no guesswork about the final payoff date

- The full promotional balance that must be cleared

- Whether payments need time to process before they post

- What happens if any amount remains after the promotion ends

Why transparency matters

National advice on financing often feels cold and generic. It warns shoppers away from everything or tells them all financing is fine if they're “responsible.” Neither approach is very helpful when someone is standing in a showroom trying to furnish a real home.

A better approach is straightforward. Promotional financing can be useful. It can also be expensive if the rules are misunderstood. The smart move is to treat the deadline as firm, calculate the payoff before the purchase is made, and make sure the offer supports the household budget rather than stretching it.

Applying for Financing at the Gorins Showroom

For many shoppers in Norwich, Plainfield, Waterford, and nearby Eastern CT communities, the financing process feels intimidating before it starts. In practice, the in-showroom experience is usually much simpler when an associate walks through it step by step.

What the process usually looks like

A shopper typically begins after choosing the furniture or mattress they want to purchase. That might be a sofa from Flexsteel, a custom piece from the F9 Custom Sofa series, or a bed from The Sleep Gallery featuring brands such as Tempur-Pedic, Serta, or Beautyrest. Once the product selection is clear, the financing conversation becomes much easier because the total purchase is known.

An associate can then help the shopper review available promotional options through partners such as the Nest Credit Card issued by Comenity Capital Bank and TD Bank. The point isn't to rush anyone through paperwork. It's to match the financing structure to the shopper's comfort level and payoff plan.

Shoppers who want a preview can review the current Gorins financing information before visiting.

Questions worth asking at the counter

The smoothest applications happen when shoppers ask practical questions right away. Helpful ones include:

- Is this deferred interest or equal monthly payments so the repayment structure is clear

- Can this offer be used on custom furniture or mattresses if the purchase includes made-to-order items

- When does the promotional period begin because timing affects payoff planning

- How are payments made after approval so there's no confusion once the furniture is home

A financing application should feel like a conversation, not a test.

Why local guidance helps

Local showrooms offer a distinct advantage. A Norwich-area shopper can sit down with someone, review the terms, and ask follow-up questions in plain language. That matters when someone is choosing among custom dining, reclining furniture, or a mattress built around comfort by feel and healthier sleep.

It also helps shoppers think beyond approval. A family furnishing a room should know whether the payment schedule fits around rent, mortgage, school expenses, and seasonal household costs. Financing works best when it supports the home, not when it competes with every other bill in it.

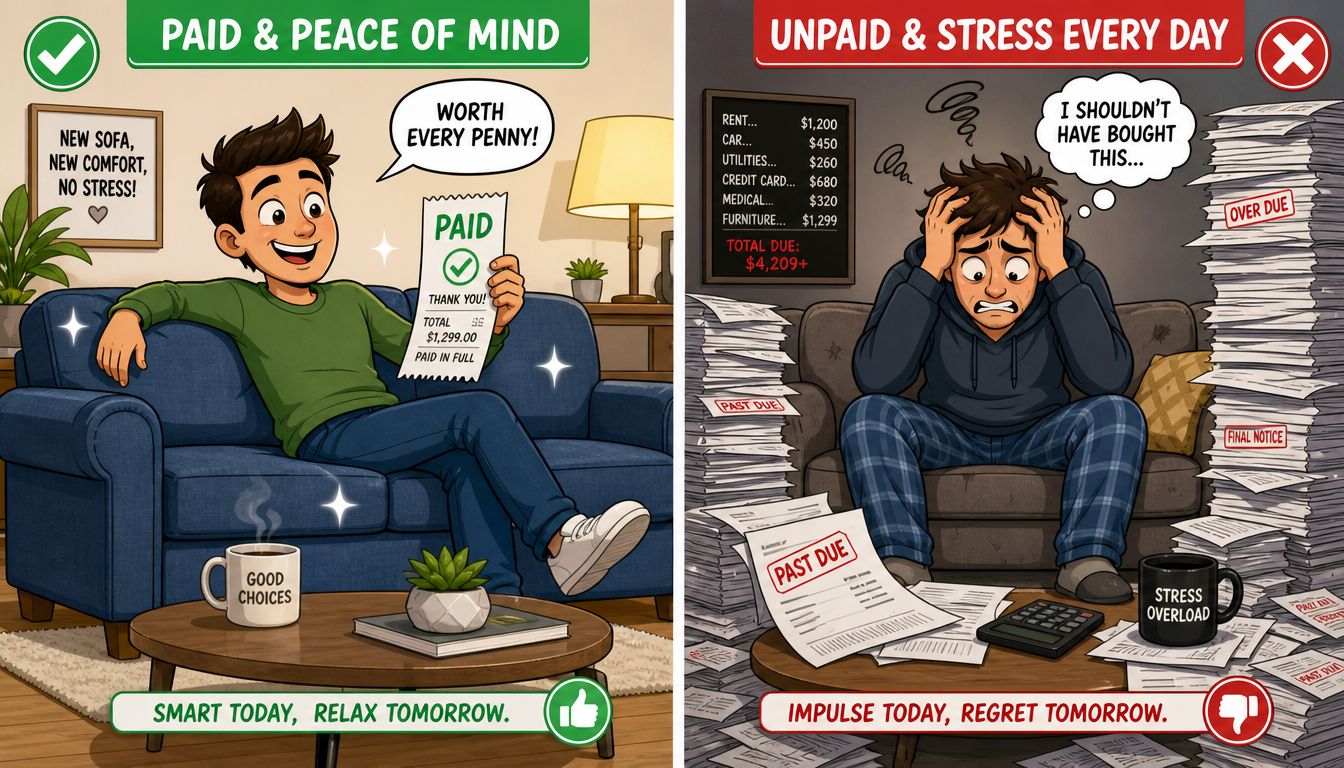

A Tale of Two Shoppers A Repayment Example

Stories make this topic easier to understand than definitions alone. Consider two shoppers who both buy a custom F9 Series sofa using a 90 days same as cash furniture promotion.

Shopper A uses the promotion as a plan

The first shopper treats the offer like a short runway. Before taking the sofa home, the shopper divides the purchase total into equal chunks and schedules those payments across the promotional window. Each payment is large enough to reduce the balance on purpose, not just satisfy the minimum due.

Because the shopper finishes paying the balance before the deadline, the promotion does exactly what it promised. The sofa comes home now, the budget stays organized, and the account doesn't create an interest surprise later.

This is the ideal use of deferred interest financing. The offer isn't replacing affordability. It's creating timing flexibility.

Shopper B follows the minimum payment only

The second shopper assumes the minimum payment is the safe path. The account stays current, so everything seems fine month after month. The problem shows up at the end of the promotional window, when a balance still remains.

At that point, the shopper may learn the expensive part of deferred interest. Staying current isn't the same as paying the promotional balance in full. If the terms say interest applies when the deadline is missed, even by a small remaining amount, the cost of that sofa can jump fast.

The dangerous phrase in furniture financing isn't “same as cash.” It's “I thought the minimum payment was enough.”

The lesson behind the contrast

Both shoppers brought home the same style of furniture. Both used the same promotion. The difference wasn't luck or income level. It was strategy.

A shopper can usually protect the value of a short-term financing offer by doing three things well:

- Calculating the payoff in advance instead of guessing later

- Paying toward the full balance rather than drifting along on minimums

- Finishing early so processing delays don't turn into a deadline problem

This matters even more on custom orders. A made-to-order sofa or dining set is often a more intentional purchase. With thousands of combinations available through programs like Canadel Custom Dining and the F9 Custom Sofa series, the financing plan should be just as intentional as the design choice.

For our neighbors in Norwich and New London, that's the key takeaway. Promotional financing rewards precision. It punishes assumptions.

Comparing Your Furniture Financing Options

Not every shopper should choose the same path. The right financing option depends on how quickly the balance can be paid, how much monthly room exists in the household budget, and whether the purchase is a need-now item or a slower project.

Furniture Financing Options at a Glance

| Financing Type | Best For | Key Risk |

|---|---|---|

| Deferred interest promotion | Shoppers who can pay the full balance within the promotional window | Interest may apply if the balance isn't paid in full by the deadline |

| Equal monthly payment plan | Shoppers who want predictable structure for a larger purchase | Missing the payment rhythm can create budget strain |

| Layaway | Shoppers who prefer to avoid credit and don't need the item immediately | The furniture usually isn't taken home until the balance is completed |

| Lease-to-own | Shoppers who need another path to furnish a home now | Total cost and terms need careful review before signing |

When deferred interest makes sense

A short same-as-cash offer fits best when the shopper already knows where the payoff money is coming from. That could be a series of planned paychecks, a seasonal bonus already expected, or a clear amount set aside in the monthly budget.

It's less ideal for shoppers who need a long runway or who aren't sure they can clear the balance on time. In those cases, the structure may feel helpful at first but become stressful later.

Where equal monthly payments can help

Some larger home projects need more breathing room. A full-room refresh, a premium mattress upgrade, or a custom dining order may be easier to manage under a promotional financing plan with equal monthly payments. That format is often easier for budget-minded households because the payment target is more predictable from the beginning.

Readers looking at more flexible approval paths can explore furniture financing guidance for challenged credit situations.

Some shoppers save money with the shortest plan. Others sleep better with the most predictable one.

Why one size doesn't fit every home

Layaway can still work for shoppers who want to avoid taking on any financed balance and don't mind waiting. Lease-to-own may help when immediate furnishing matters most, but the terms deserve careful attention before commitment.

A local design-focused showroom should help customers compare these paths without pressure. That matters for a wide range of purchases, from Living Room Furniture in Eastern CT to Canadel Furniture in Connecticut to mattresses chosen by comfort by feel. The best answer is the one that supports the room and the budget at the same time.

Your Checklist for a Truly Interest-Free Purchase

A short promotional offer can be useful, but only when the shopper manages it actively. The easiest way to stay in control is to decide the payoff plan before the order is placed.

A simple checklist that keeps surprises away

Read the exact promotion terms: A shopper should know whether the offer is deferred interest or equal monthly payments. Those two structures can sound similar in conversation but behave very differently in real life.

Set reminders before each due date: Calendar reminders work best when they're scheduled a few days early, not the night before. That gives time to fix a login issue, bank delay, or simple oversight.

Pay a fixed amount, not just the minimum: The minimum due is usually designed to keep the account current. It usually isn't designed to erase the promotional balance by the deadline.

Aim to finish early: Paying the account off before the last possible day leaves room for payment posting time. That extra cushion can protect an otherwise well-planned purchase.

Review the paperwork with a store associate: A shopper should leave the showroom knowing the due dates, the payoff target, and how payments will be made after purchase.

Practical rule: If a shopper can't explain the payoff plan in one sentence, the plan isn't clear enough yet.

The calm way to use financing

The best furniture financing decisions don't feel dramatic. They feel organized. A household sees the room it wants, chooses the quality it wants, and matches that purchase with a payment schedule that won't create stress later.

That approach works especially well for custom pieces and mattresses, where the goal isn't bargain hunting. It's long-term comfort, value, and a home that feels thoughtfully put together.

Your Local Furniture Financing Questions Answered

Can promotional financing be used on custom dining or custom sofas

That depends on the current promotion and the purchase details, so a shopper should ask before ordering. In many cases, financing may apply to custom programs, including Canadel Custom Dining and the F9 Custom Sofa line. Since these pieces offer thousands of combinations, it's smart to confirm the financing terms at the same time the design details are finalized.

Can financing be used for mattresses too

Often, yes. Mattress shoppers looking at The Sleep Gallery may be able to use promotional financing on brands such as Tempur-Pedic, Serta, and Beautyrest, depending on the current offer and approval. For many households, this is especially helpful because sleep purchases tend to be need-based rather than optional.

What's the difference between store financing and the bank partner

The showroom helps present the offer and application, but the financing account itself is typically provided by a lending partner such as Nest Credit or TD Bank. That means the shopper buys locally and gets local guidance, while the credit account, payment processing, and account servicing are handled by the financing partner.

Is approval the only thing that matters

No. Approval matters, but fit matters more. A shopper should look at the payment plan, the promotion type, and the payoff timeline before deciding. A financing offer only helps when it supports the household budget.

Where can local shoppers go to get help in person

Shoppers in Norwich, New London, Plainfield, Waterford, and nearby communities can review showroom information through the Gorins location page. In-person help is useful when someone wants to compare furniture, comfort-test mattresses, or ask detailed questions about financing terms before bringing anything home.

Since 1936, Gorins Furniture & Mattress has helped Norwich and Eastern CT families create homes they love. From custom-designed Canadel dining sets to the latest in Tempur-Pedic sleep technology, they combine a massive selection with the personalized care only a local, family-owned business can provide. Visit the Norwich showroom, take the online Style Quiz, or browse the Clearance section for value-driven savings and 5-Star Delivery service.